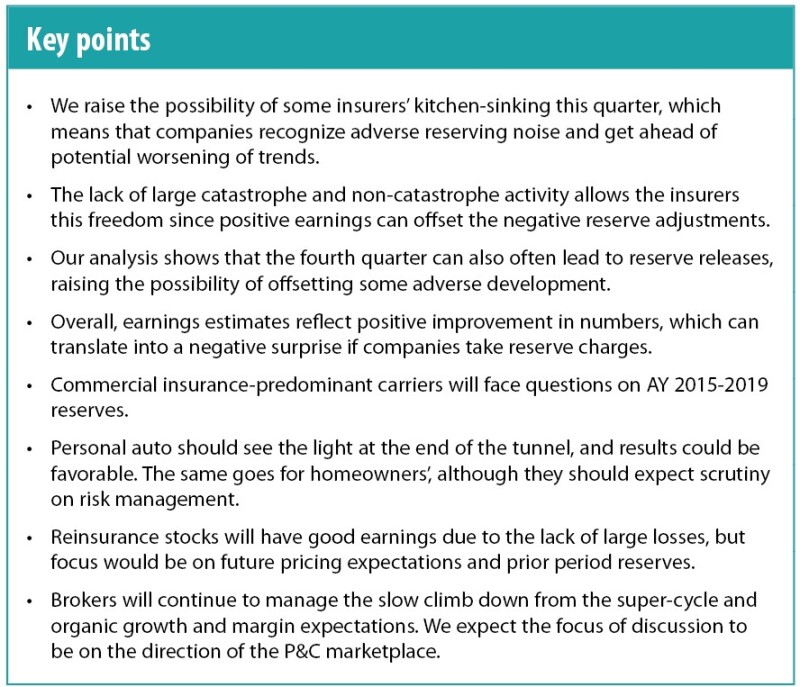

The shortage of serious disaster exercise within the fourth quarter of 2023, regardless of one other 12 months of energetic losses total, signifies that outcomes would probably be extra favorable in comparison with earlier quarters. In principle, this permits the trade to trim this quarter to remain forward of future developments and construct a further reserve buffer for earlier years.

The flip facet of this argument is that any crash might put short-term strain on shares that had already underperformed the S&P in 2023.

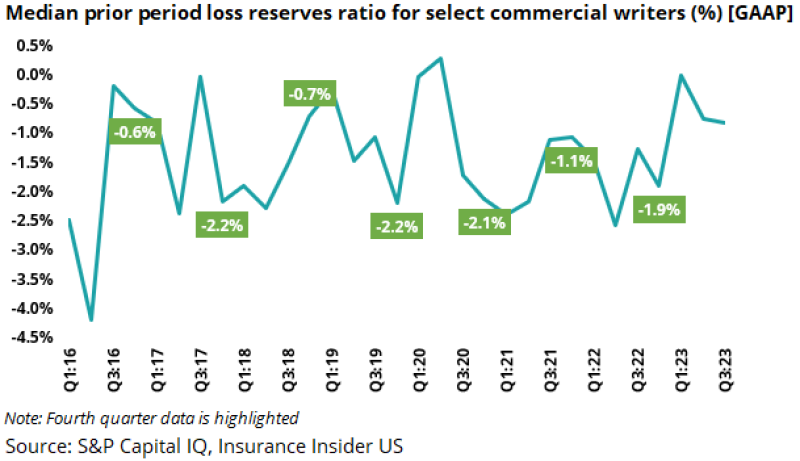

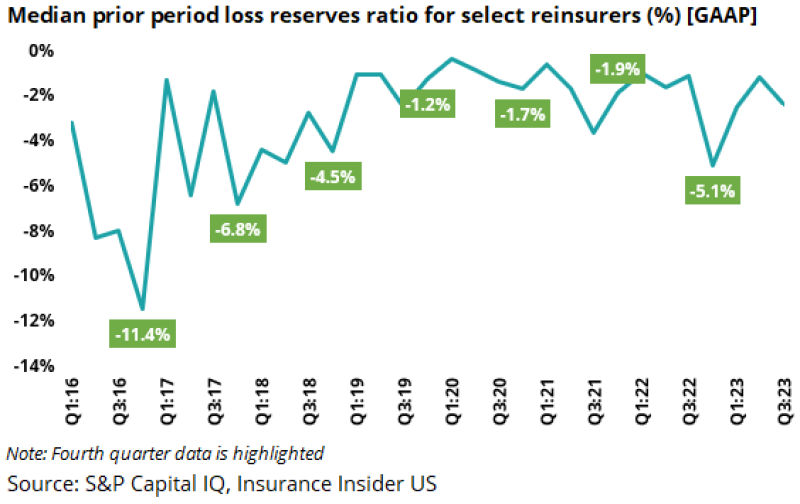

The chart under exhibits prior interval releases for the choose group of economic companies corporations, with fourth quarter releases highlighted. What’s noticeable is that fourth quarter releases are increased in lots of intervals than within the different intervals.

This makes intuitive sense for the reason that fourth quarter usually contains year-end outcomes, which requires a extra complete accrual assessment. Subsequently, we might not be shocked if some corporations used this quarter as a chance to take the bitter medication of reserve changes first.

Nevertheless, the fourth-quarter 2023 Avenue estimates proven under seem like on a barely constructive development, reflecting a quieter catastrophe quarter. This creates room for a damaging shock as corporations make reserve changes this quarter.

The calendar under exhibits the schedule of fourth-quarter earnings reviews, with Truist and Vacationers main the best way and setting the stage for early tendencies.

Generally, we anticipate the next key themes by sector:

Business traces:

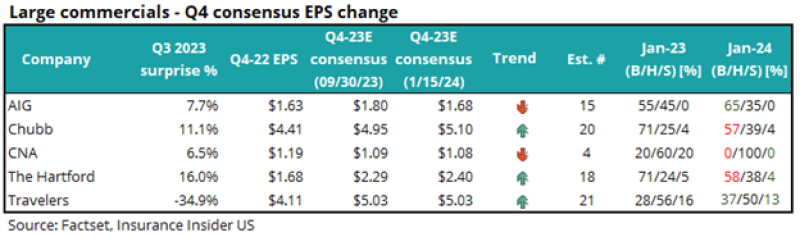

Anticipate renewed dialogue about loss reserves for fiscal 12 months 2015-2019 and the way corporations consider their loss choices. As well as, the same old subjects of social inflation, rate of interest will increase and basic financial developments are in focus.

Private traces:

Will this be the quarter? If Progressive’s month-to-month outcomes are any indicator, this quarter might be the one the place we lastly begin placing the noise within the rearview mirror. On the house owner facet, discussions about tendencies and nationwide measures might be anticipated. Moreover, the outcomes might be higher as loss exercise was at a decrease stage.

InsurTech:

The whack-a-mole continues, with corporations reconciling development, capital and loss tendencies. As brief curiosity stays excessive, risky inventory reactions to earnings are anticipated.

Reinsurance:

Though the January 1 renewal was robust, it probably fell wanting preliminary expectations. Just like business questions, anticipate questions concerning the adequacy of reinsurance reserves in legal responsibility insurance coverage. As a result of lack of main loss exercise, we anticipate a great quarterly reporting season.

Florida:

We anticipate the dialogue to proceed relating to new entrants and the general well being of the sector. Outcomes are anticipated to be robust given the low regional losses.

Property brokers:

As a primary derivation, anticipate questions concerning the longevity of the cycle. Additionally anticipate in depth discussions about how this smooth financial touchdown will proceed. Natural development figures are more likely to be good, though they may present a downward development.

We discover these concepts under.

Commercially:

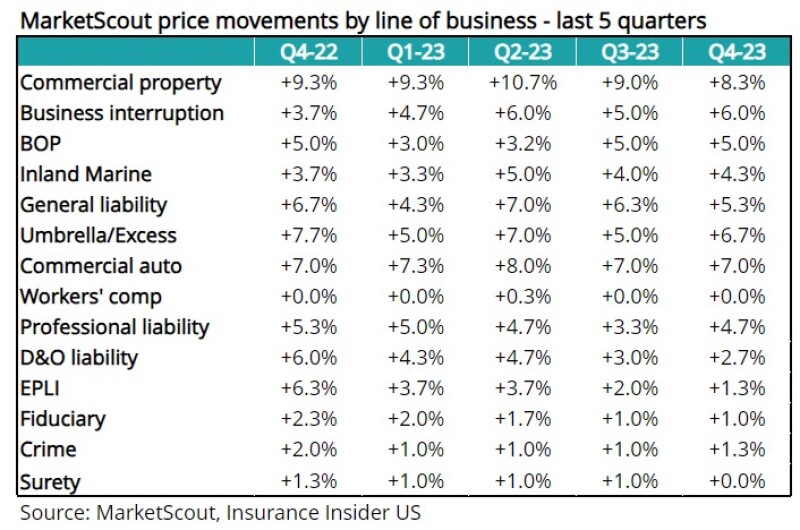

Present worth information exhibits a continuation of the tendencies noticed in earlier quarters with sporadic sequential declines, which isn’t stunning. Nevertheless, the main focus ought to be on making certain that these pricing numbers translate into revenue and ROE development.

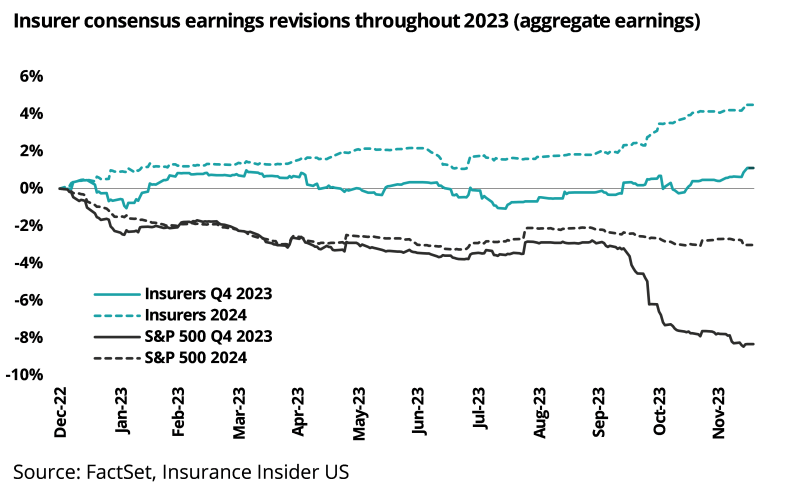

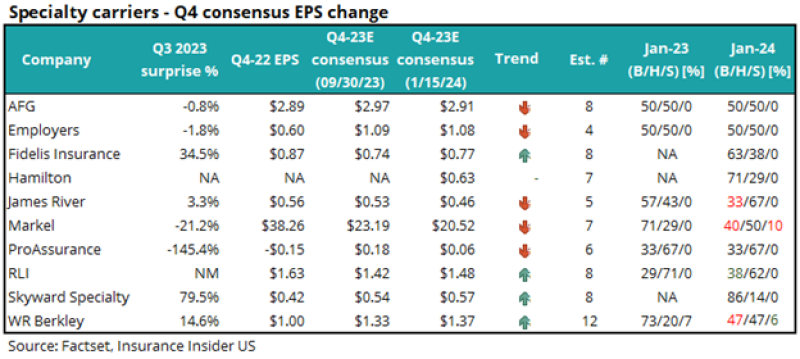

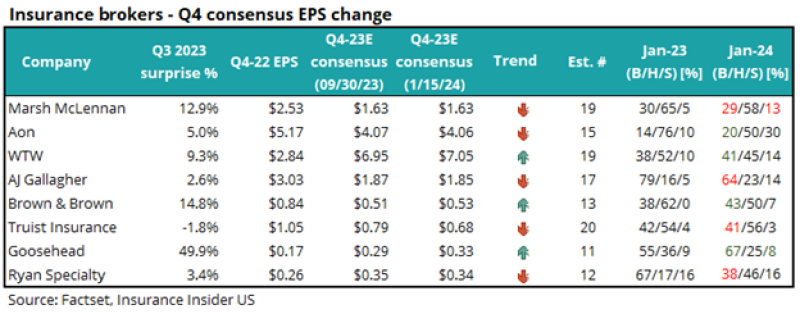

The chart under exhibits forecast fourth-quarter earnings per share as of this week and likewise exhibits the identical quantity about 100 days in the past. Whenever you take a look at the cohort, the image is blended. We added two columns this quarter to characterize Avenue Sentiment, which compares the share of analysts who’ve referred to as to purchase/maintain/promote the inventory. This exhibits an total damaging development in comparison with the earlier 12 months.

We have now added charts to this preview exhibiting the median reserves efficiency for the group. As proven under, the fourth quarter usually seems to be a interval of reserve liquidation, which feeds again to our place that we might not be shocked to see corporations make the most of the chance to take reserve measures.

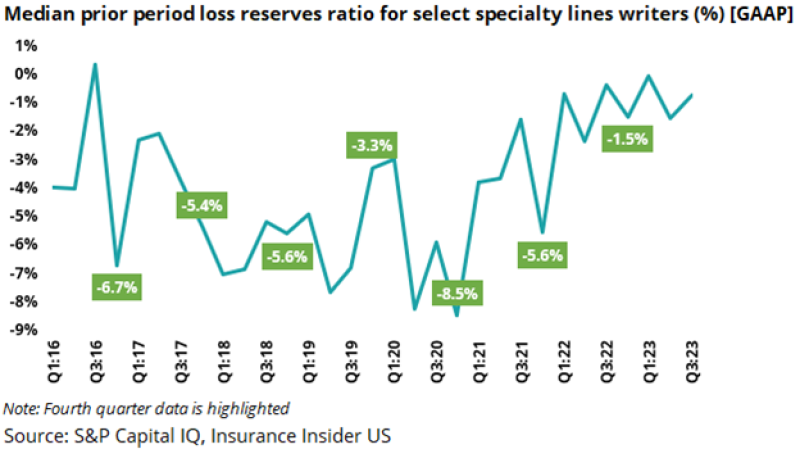

The specialty sector under exhibits an identical development, with half of the road estimates rising.

As with the business gamers, the next desk exhibits the common reserve clearances for the specialty gamers. Specialist gamers clearly have higher managed reserves, resulting in increased releases over time. We anticipate decrease reserve volatility on this sub-segment.

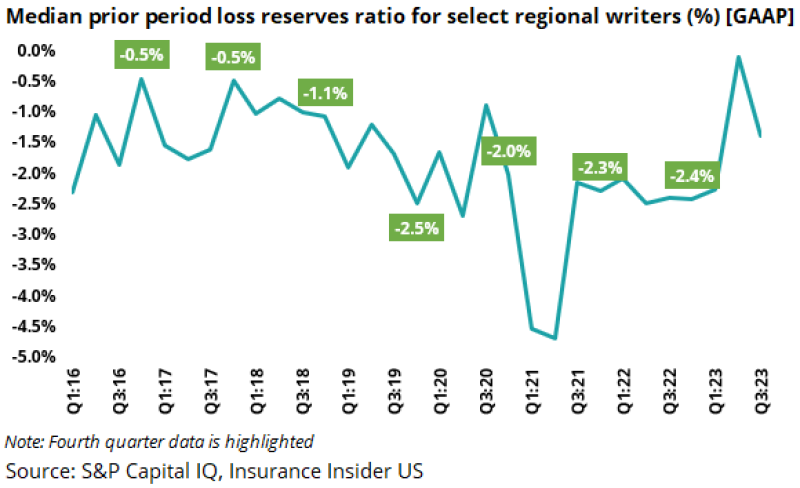

An analogous blended development is anticipated to emerge throughout the regional house, though we might notice the constructive bias in scores for 2024 versus 2023.

An attention-grabbing development might be seen when common releases over time. These seem to have elevated as regional suppliers have demonstrably improved the standard of their books. We anticipate much less cleansing effort on this space.

Reinsurance:

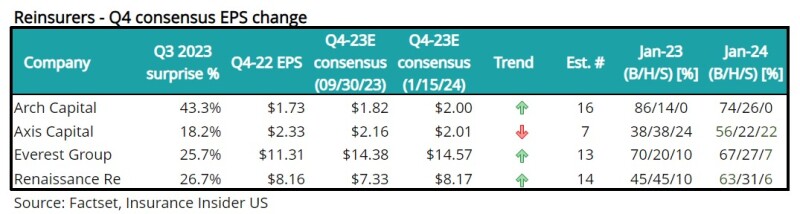

Reinsurers’ earnings have largely been revised upward for the reason that finish of the third quarter, reflecting lower-than-expected disaster losses. Latest brokerage reviews counsel a great, if barely disappointing, 1/1 renewal. We anticipate the convention calls to concentrate on the April 1 and July 1 renewals and obtainable capital assets.

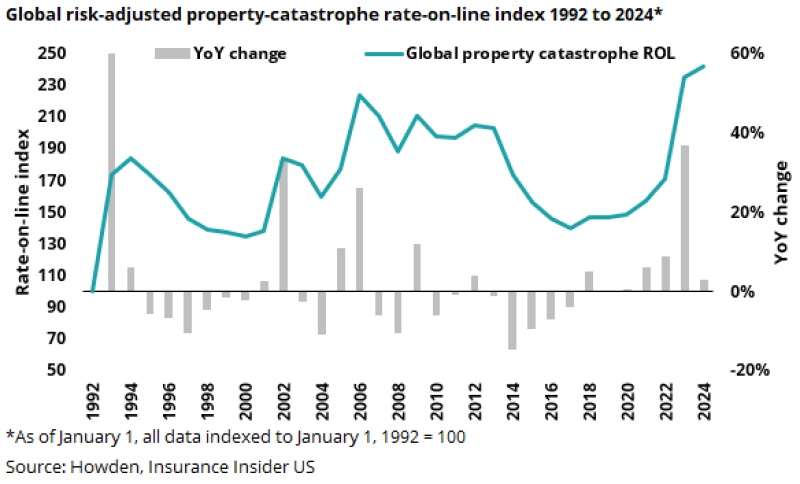

The chart under exhibits ROL, which has elevated barely in comparison with final 12 months and remains to be at an all-time excessive.

Past rates of interest and catastrophes, reserve changes are the subjects we anticipate to see extra coloration on on earnings calls and convention calls. Traditionally, this group has benefited from a bigger variety of publications. Moreover, some corporations can also take into account reserve changes to their insurance coverage contracts in the course of the quarter, given the shift to a balanced enterprise portfolio that features insurance coverage and reinsurance.

Florida Home Employees:

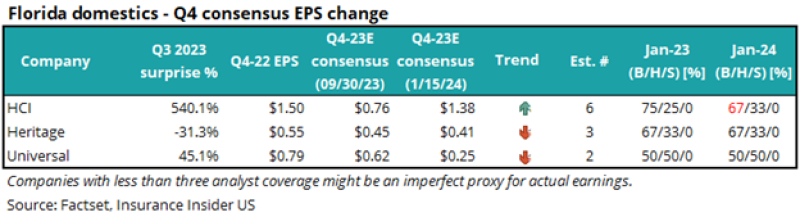

This group had a comparatively good 12 months as a result of hurricane injury couldn’t be outlined in comparison with earlier years. We will see this within the shift in HCI’s earnings estimates over the past 90 days or so.

We anticipate feedback on the convention name to concentrate on the impression of recent market entrants, together with mutual members.

Private traces:

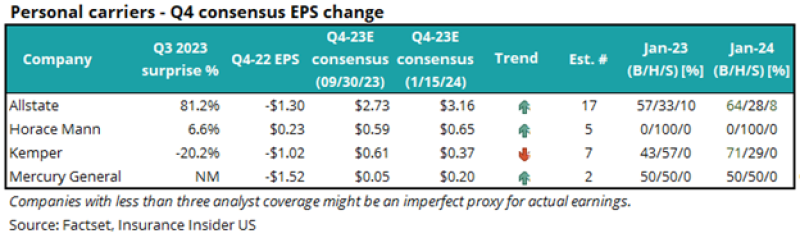

Though most of 2023 has been harder for a number of franchises, it looks like we’re seeing the sunshine on the finish of the tunnel. The estimate abstract confirms this, other than Kemper persevering with to handle challenges on the franchise stage.

Private automotive

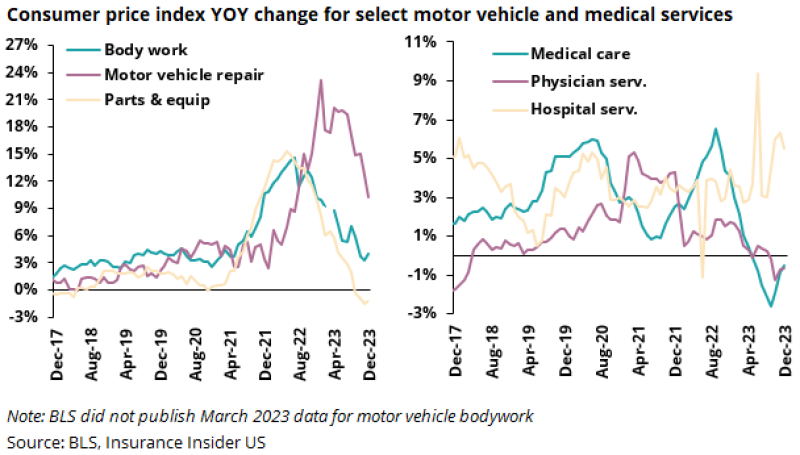

Final week, the newest BLS/CPI information confirmed continued moderation on a number of critical points, as proven under, and we anticipate feedback on the decision to bolster this.

The rest of the 12 months will concentrate on authorities and tariff actions wanted to widen the hole between pricing and loss prices.

Home-owner

As mentioned in our outlook, related underwriting actions occurred within the house owner sector, together with exits and withdrawals on the state stage. The larger problem stays the elevated ranges of losses, together with from SCS, that we’ve seen lately. We subsequently assume that traders will place higher scrutiny on this enterprise space.

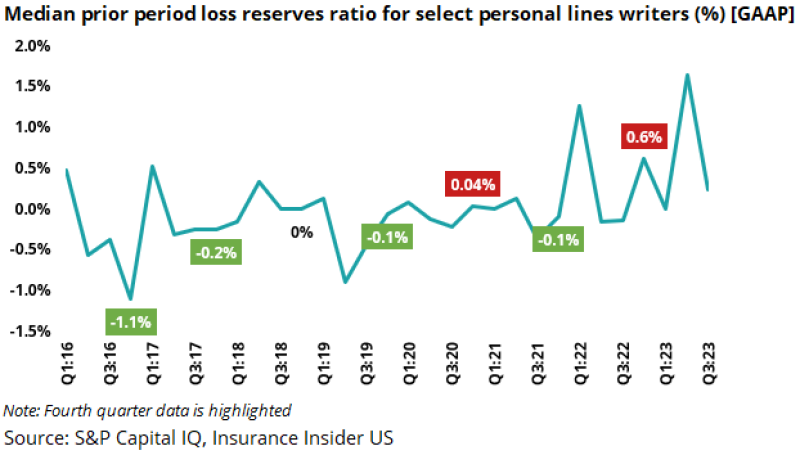

The chart under exhibits common reserve releases on a quarterly foundation. Be aware the unfavorable efficiency proven in purple in comparison with different sectors proven above. The damaging improvement has tended to lower as noise from non-public automobiles normalized within the earlier interval. We assume that the damaging improvement shall be much less extreme this quarter.

Property brokers:

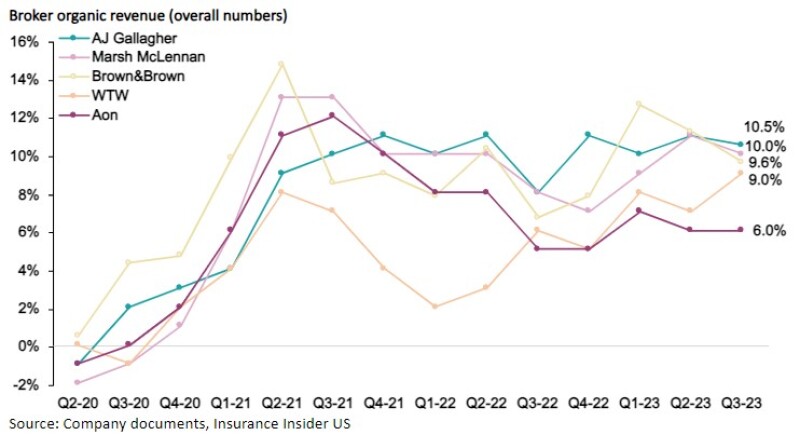

As main indicators, brokers are at an attention-grabbing level within the insurance coverage cycle. They’ve proven vital natural development and margin growth, however that is beginning to sluggish.

Suppose promoting writers are discussing the restoration of reserves within the earlier interval and the ensuing slowdown of their gross sales. Will brokers be capable to transfer away from the overarching dialogue and proceed to forecast robust natural development?

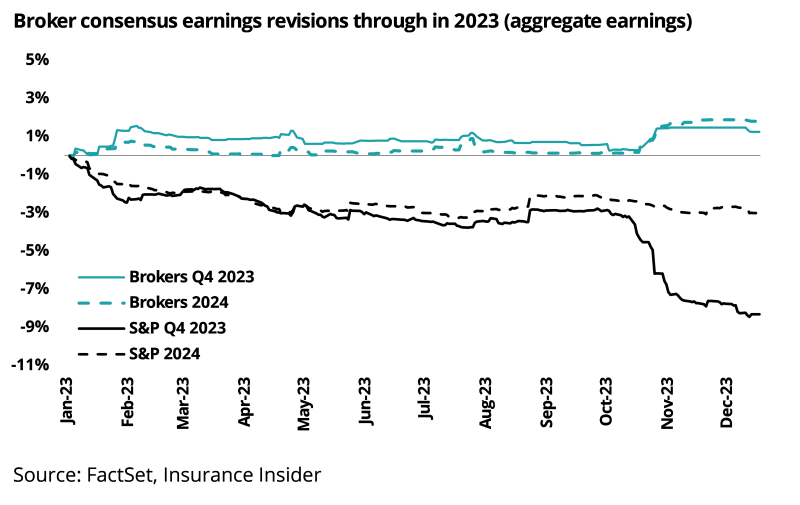

General, total earnings expectations remained unchanged, whereas S&P noticed a downward development.

On an organization foundation, the estimates present a 50/50 cut up with slight deviations in both course.

We had been beforehand pleasantly shocked as to when the dealer supercycle would finish after a rebound within the first quarter of 2023, however latest quarters level to an orderly rise.

In abstract, the fourth quarter presents a chance for commercially predominant authors to scale back their reserves and put together for the potential for future reserve changes for the 2015-2019 fiscal 12 months. If we do not see any reserve changes, this space ought to have a great quarter because of the lack of main loss exercise.

As for private prospects, auto insurance coverage could lastly mirror the sunshine on the finish of the tunnel, whereas owners will take into account continued corrective motion. Outcomes will once more profit from a scarcity of enormous SCS and different non-catering exercise within the fourth quarter.

Though quarterly outcomes for reinsurers shall be good, the main focus shall be on future tariff expectations and any reserve changes for hybrid insurance coverage.

Brokers’ outcomes will mirror the same old balancing act between basic financial situations and expectations of a sluggish decline from peak natural development charges.